Blockchain is a technology that underpins the success of Bitcoin and other digital currencies. Wall Street is particularly interested in blockchain: The elimination of manual processes around reconciliation with customers, trading partners, and securities exchanges using blockchain is projected to save banks nearly $20 billion annually by 2022.

Blockchain has uses beyond financial transactions to improve the security and efficiencies of a range of business activities such as applications requiring transparency on data and documents with a permanent time and date stamp. In insurance, for example, blockchain technology can be used for customer onboarding, smart contracts, and fraud detection. In manufacturing, blockchain is being used in supply chain applications and 3D printing.

To better understand blockchain, let’s first look at why blockchain is so important and how it ensures the integrity and efficiency of the Bitcoin network. Then, we will look at how Acronis provides a solution that uses blockchain to record and protect the authenticity of your business assets.

What is blockchain?

McKinsey defines blockchain as “a distributed register to store static records and/or dynamic transaction data without central coordination by using a consensus-based mechanism to check the validity of transactions.” When you pay a bill — your mortgage for example — a third party such as a bank or mortgage company manages the transaction. Blockchain is a technology that creates a distributed and scalable digital ledger of transactions. It removes the need for a central authority while keeping the transaction highly secure. Here’s how it works.

In the Bitcoin case, each computer connected to a Bitcoin network – called a node – automatically downloads a copy of blockchain, which is used to validate, relay, and record a transaction by generating a “block.” Every block is stored in the blockchain in a linear, timestamped, and chronological order. In addition, every block contains a copy of the previous block, which verifies data authenticity.

The evolution of blockchain

We are only in the early adoption stages of blockchain technology. Along with its use for Bitcoin, leading organizations are beginning to use blockchain for certain asset classes and to meet specific regulatory requirements. According to MarketsandMarkets, the global blockchain technology market will grow from US$ 210.2 million in 2016 to US$ 2,312.5 million by 2021, at a Compound Annual Growth Rate (CAGR) of 61.5 percent.

While many blockchain applications are aimed at banking and ecommerce, any transaction requiring data immutability and the need to preserve the integrity of original data can take advantage of blockchain technology. This is why Acronis recently announced its latest version of Acronis Storage — a universal software-defined storage solution that incorporates Acronis Notary™ with blockchain.

Acronis Notary™ with blockchain

There are many cases where authenticity of data and documents is very important, if not critical in businesses, institutions, and government agencies. These organizations have intellectual property assets, contracts, property registry documents, medical files, chain-of-evidence documents, security camera footage, archived documents subject to audit, and other key data and sensitive documents.

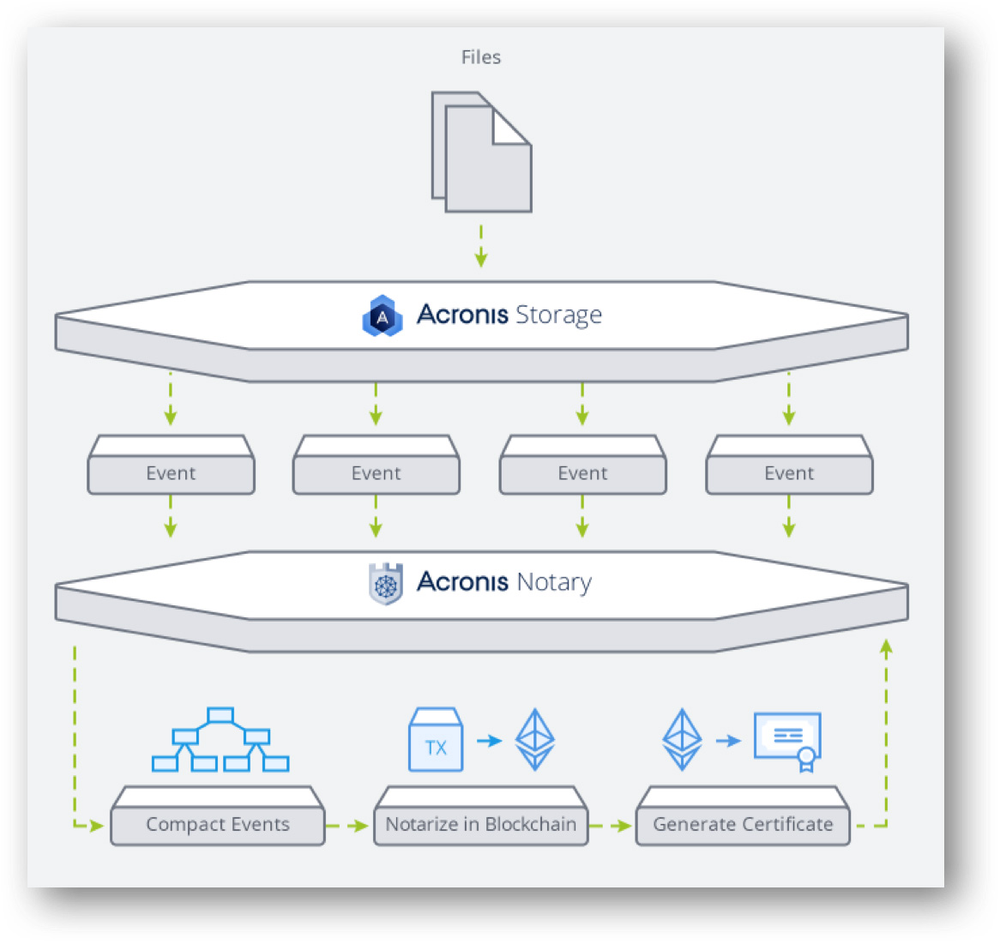

Acronis Storage includes integration with Acronis Notary™ to leverage blockchain to ensure the authenticity of data. The diagram below illustrates how Acronis Notary™ works.

When data, a file, or a document is stored in Acronis Storage, Acronis Notary™ creates a “fingerprint” — a hash for each file. A hash is an algorithm that turns data into an output of fixed length – a fingerprint.

The hash is timestamped and recorded in blocks into the blockchain. Each block includes the previous block’s hash and it references the previous hash it is building upon. The blockchain is then distributed so that if any location that holds a copy of the blockchain is compromised, other locations can continue to maintain it. Every record in the blockchain is now immutable and independently verifiable; furthermore, notarization records cannot be manipulated. When required, authenticity of data can be verified by comparing two fingerprints of the same data.

Blockchain is being hailed as the second coming of the internet and a technology that re-invents the cloud. Regardless of the hype, blockchain will be a core technology that will influence applications in the financial services, insurance, manufacturing, healthcare, government; indeed, every industry segment over the coming years. Acronis’s use of blockchain technology in Acronis Storage is yet the latest demonstration of its commitment to develop best-in-class data protection solutions for its customers. When Acronis says that your data is protected, it truly means your data is protected!

READ MORE:

About Acronis

A Swiss company founded in Singapore in 2003, Acronis has 15 offices worldwide and employees in 60+ countries. Acronis Cyber Platform is available in 26 languages in 150 countries and is used by over 21,000 service providers to protect over 750,000 businesses.